Steps In

Steps Out

Outlook

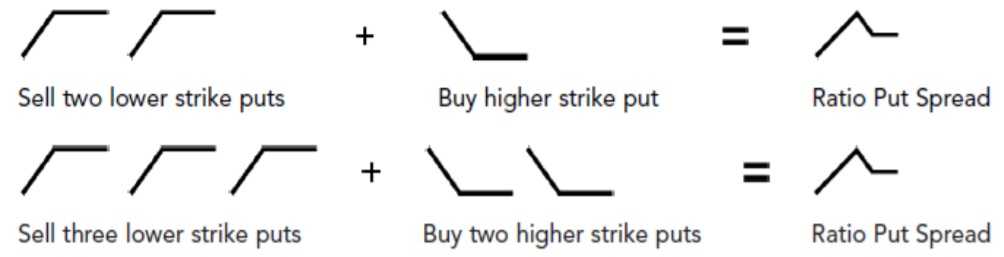

Rationale

Net Position

Effect of Time Decay

Time Period to Trade

Breakeven Down = [Higher strike] less [difference in strikes * number of short contracts] / [number of short contracts less long contracts] less [net credit received] or plus [net debit paid]

Breakeven Up = [Higher strike] – [net debit * number of long contracts]

Exiting the Position

Mitigating a Loss

Advantages

Disadvantages

Share this Content

© 2021 All rights reserved

Ask Your Query