The Long Put Synthetic Straddle involves buying puts and counteracting them with a Long Stock position.

To create the Straddle shape, we have to buy twice the number of puts.

So for every 100 shares we buy, we have to buy two put contracts, which represent 200 shares of the stock.

The Long Stock position replicates the action of buying the same number of calls as puts.

Buying stock to counteract , the long puts in this case, the Long Put Synthetic Straddle is an expensive strategy, requiring a large net debit.

Buy the stock (if you buy 100 shares for every put contract you buy).

Buy two ATM puts per 100 shares you buy.

If the current stock price isn’t near the nearest strike price, then it’s better to choose the nearest ITM strike (higher than the current stock price).

Steps to Trading a Long Put Synthetic Straddle

Steps In

Actively seek chart patterns that appear like pennant formations, signifying a consolidating price pattern.

Try to concentrate on stocks with news events and earnings reports about to happen within two weeks.

Choose a stock price range you feel comfortable with.

Steps Out

Manage your position according to the rules defined in your Trading Plan.

Exit either a few days after the news event occurs if there is no movement or after the news event if there has been profitable movement.

If the stock thrusts up, sell the stock (making a profit for the entire position) and wait for a retracement to profit from the puts.

If the stock thrusts down, sell the puts (making a profit for the entire position) and wait for a retracement to profit from the stock.

Never hold into the last month.

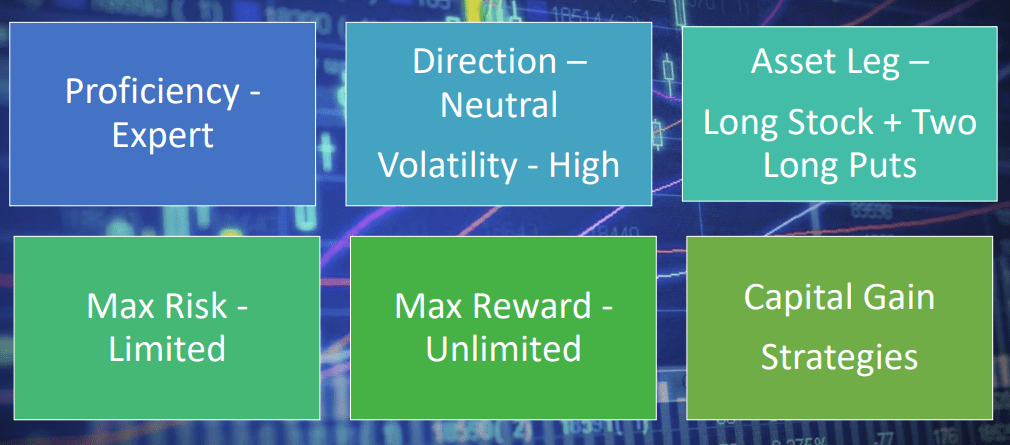

Context - Long Put Synthetic Straddle

Outlook

With a long Synthetic Straddle, your outlook is neutral in terms of direction, but you’re looking for increasing volatility in the stock so that the stock price moves beyond your breakeven points on either side.

Rationale

To execute a direction neutral trade where you expect the stock to behave with increasing volatility in either direction.

If the stock rises explosively, you will make money from your long stock position, which will rise faster than your Long Put position falls.

If the stock falls, you will profit from your Long Put position, which will increase in value faster than your long stock position loses value beyond the price you paid for the puts.

Net Position

This is a net debit trade because you are buying the stock and the puts.

Effect of Time Decay

Time decay is harmful to the value of your Long Puts.